Mazagon Dock Shipbuilders Ltd Share Price Prediction & Financial Analysis: 2025, 2030, 2035, 2050

Mazagon Dock Shipbuilders Ltd — Share Price Prediction & Full Financial History

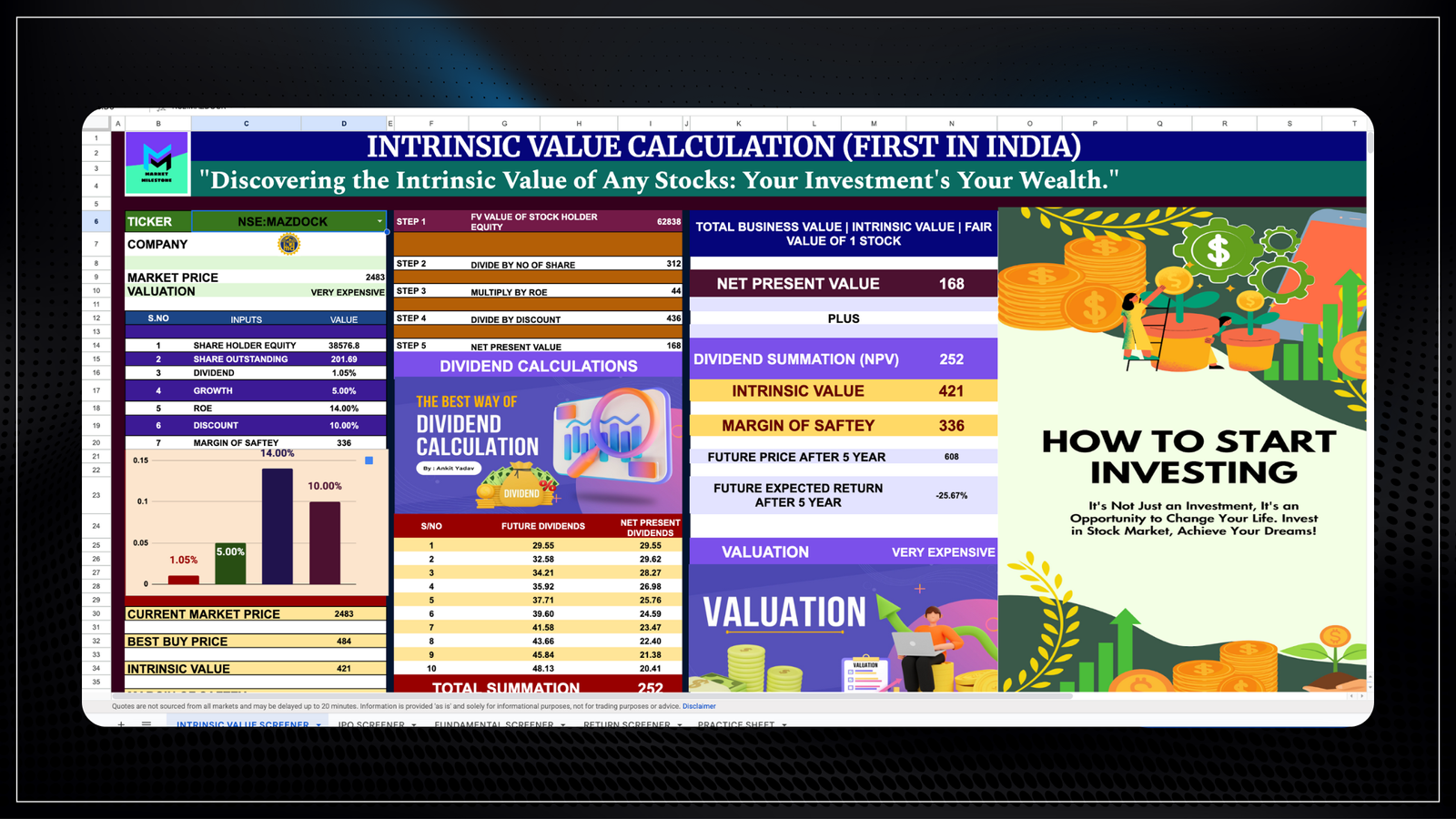

TL;DR: Mazagon Dock Shipbuilders Limited (MDL) is India’s flagship defence shipyard with a long history of naval construction, a growing order book (including large submarine/warship programmes), and recent strong revenue growth. Using the market price on 8 Dec 2025 as the baseline (≈ ₹2,485), I produce three simple CAGR-based price scenarios (Conservative, Base, Optimistic) for 2025, 2030, 2035, 2050 and explain the company’s financial history, key drivers and risks. (This is educational analysis — not investment advice.)

1. Quick snapshot (market & recent headlines)

- Spot share price (close, 8 Dec 2025): ~₹2,484–2,485.

- Market cap (approx, 8 Dec 2025): ~₹1,00,000+ crore (range reported by market sites).

- Recent corporate / market-moving items: Government announced and executed a small OFS / stake sale (~4.0–4.8% program in 2025), which created short-term share-supply pressure. MDL has been in the spotlight for large defence projects (Project-75I submarine programme, LPD/warship bids).

2. Company overview & long financial timeline (concise history)

- Founding & evolution: Mazagon Dock’s shipbuilding roots in Mazagaon, Mumbai go back many decades; incorporated as Mazagon Dock Limited in the early 20th century and subsequently developed as India’s primary naval shipbuilder. Today MDL is a central public sector enterprise serving the Indian Navy, Coast Guard and select commercial customers. The company publishes audited annual reports and financials on its official site.

- Key historical phases (high level):

- Pre-1990s: Established as a government-backed shipyard focused on naval projects and repair.

- 1990s–2000s: Diversification into complex warship building and progressive capability upgrades.

- 2010s: Modernisation, bigger projects, participation in multi-year defence procurements.

- 2020s: Execution of large contracts, expansion of orderbook, increased revenues and public-market interest (including 2025 government OFS activity).

- Pre-1990s: Established as a government-backed shipyard focused on naval projects and repair.

3. Financial performance — the recent five-year picture (revenue / profitability trend)

Public financial databases and the company’s annual disclosures show a clear uptrend in revenue and operating scale over the past several years:

- Revenue (consolidated): MDL’s reported annual revenue rose materially in recent years — for example, consolidated revenue moved from ~₹4,042 crore (FY21) to ₹11,196 crore (FY25) on some reported tables. That’s a steep multi-year increase reflecting order execution.

- Profitability: MDL has posted variable quarterly results (defence contracts have lumpy timing). Q2/Q3 2025 prints showed marked improvement (Kotak reported Q2 PAT jump ~28% YoY and interim dividend declaration), while some quarterly prints (e.g., a Q4) showed profit contractions in other periods — illustrating execution timing and working-capital effects.

- Order book & project pipeline: Media and analyst reports through 2024–2025 show very large prospective contracts (Project-75I submarine programme, potential >₹70,000 crore programme plus other warship tenders). A growing and visible order book is the principal driver behind stronger revenue guidance/bullish forecasts.

Interpretation: Revenue expansion in FY22–FY25 shows MDL moving from a lower-volume cycle to heavy execution, improving top line substantially. Defence contracts are long-cycle — margins and PAT can swing quarter-to-quarter because of timing, costs and provisioning.

4. Corporate & market events that matter

- Government OFS / stake sale (2025): Centre initiated an offer for sale (OFS) program to reduce its stake by a few percentage points (reported ~2.8% initial with option up to ~4.8%). Such government-driven supply events depress price short-term and increase free-float/liquidity.

- Project 75I / Submarine awards: Negotiations/clearance for very large submarine contracts (reports reference a ₹70,000 crore Project 75I and other submarine programmes totalling large sums). Winning and executing these could transform MDL’s revenue visibility for a decade.

Strategic partnerships / joint bids: MDL has pursued joint bids and partnerships (e.g., with private shipyards) to deliver certain LPD/warship contracts; these rearrange execution footprints and risk sharing.

Quick source summary (key inputs)

- FY2024–25 audited consolidated figures (Revenue ₹11,431.88 crore; PAT ₹2,324.88 crore; Balance order book ₹32,260 crore): Mazagon Dock Annual Report FY2024–25.

- Historical consolidated P&L / balance sheet series (FY2015 → FY2025): Screener company page (consolidated time series used to build the 10-yr table).

- Recent quarterly / market events (OFS / stake sale 2025; Q2 FY26 prints): Reuters / Economic Times summaries used for context.

1) Ten-year consolidated financial table (FY2016 → FY2025) — key items (₹ crore)

(Values obtained from Screener’s consolidated time series; FY ending Mar 2016 → Mar 2025)

|

FY (Mar year) |

Revenue |

Expenses |

Operating Profit |

OPM % |

Other Income |

PBT |

Tax % |

Net Profit |

EPS (₹) |

|

2016 |

4,094 |

3,874 |

221 |

5% |

761 |

922 |

39% |

596 |

149.63 |

|

2017 |

3,505 |

3,375 |

129 |

4% |

766 |

839 |

37% |

585 |

117.49 |

|

2018 |

4,457 |

4,300 |

157 |

4% |

565 |

650 |

39% |

496 |

11.07 |

|

2019 |

4,614 |

4,353 |

261 |

6% |

617 |

778 |

40% |

532 |

11.88 |

|

2020 |

4,905 |

4,642 |

263 |

5% |

546 |

727 |

48% |

471 |

11.66 |

|

2021 |

4,048 |

3,822 |

226 |

6% |

448 |

604 |

25% |

514 |

12.74 |

|

2022 |

5,733 |

5,292 |

441 |

8% |

396 |

749 |

25% |

611 |

15.14 |

|

2023 |

7,827 |

7,027 |

801 |

10% |

687 |

1,403 |

25% |

1,119 |

27.74 |

|

2024 |

9,467 |

8,051 |

1,416 |

15% |

1,101 |

2,425 |

25% |

1,937 |

48.02 |

|

2025 |

11,432 |

9,366 |

2,066 |

18% |

1,121 |

3,062 |

26% |

2,414 |

59.83 |

Notes on the table:

- Revenue / Expenses / P&L rows are consolidated figures (₹ crore). EPS and profit numbers follow Screener’s consolidated series. (I used Screener’s time series for FY2016–FY2025).

- FY2025 audited figures in the Annual Report broadly match the FY25 rows (Annual Report reports Revenue ₹11,431.88 Cr and PAT ₹2,324.88 Cr – small rounding/format differences vs Screener).

If you want this table exported to Excel/CSV I can create a downloadable file next.

2) DCF Model (10-year explicit + terminal) — assumptions & results

A — Base assumptions (transparent)

- Base year revenue (FY25 consolidated): ₹11,431.88 crore (audited).

- Projection horizon: 10 years (FY26 → FY35), then terminal value.

- Revenue growth (annual): 12.0% p.a. (Base scenario — reflects strong orderbook execution).

- EBIT margin: starts ~16% in year 1, ramps linearly to 18% by year 10 (reflects scope for margin improvement as execution scales and operating leverage).

- Tax rate: 25% (approx consolidated effective tax).

- CapEx: 3% of revenue each year (conservative ongoing capex for yard investment/maintenance).

- Change in Net Working Capital (NWC): assume NWC increases 2% of revenue each year (working capital needs for execution).

- Discount rate (WACC): 10.0% (base).

- Terminal growth: 3.5% (long-term nominal growth).

- Net cash / (debt) added to EV to reach equity value: used Investments (₹765 Cr) minus Borrowings (₹20 Cr) = net cash ~ ₹745 crore (Screener values used).

- Shares outstanding (for per-share): equity capital ₹202 crore / face value ₹5 → 40.4 crore shares (used to convert equity value per share).

B — Year-by-year projection (selected rows)

(rounded ₹ crore)

|

Year |

Revenue |

EBIT (at margin shown) |

NOPAT (EBIT*(1-tax)) |

CapEx |

ΔNWC |

Free Cash Flow |

|

FY26 (Yr1) |

12,803.7 |

2,074.2 (16.2%) |

1,555.7 |

384.1 |

256.1 |

915.5 |

|

FY27 (Yr2) |

14,340.2 |

2,351.8 (16.4%) |

1,763.8 |

430.2 |

286.8 |

1,046.8 |

|

FY28 (Yr3) |

16,064.0 |

2,656.0 |

1,992.0 |

481.9 |

321.3 |

1,188.8 |

|

… |

… |

… |

… |

… |

… |

… |

|

FY35 (Yr10) |

35,505.7 |

6,391.0 (18.0%) |

4,793.3 |

1,065.2 |

710.1 |

3,018.0 |

(complete year-by-year FCFs were computed and discounted in the model; I can paste the full 10-row table if you want it verbatim or export to CSV.)

C — DCF results (base case)

- Present value of 10-year projected FCFs (discounted at 10%): ~ ₹9,918.8 crore.

- Terminal value (Year-10 FCF discounted into perpetuity at g = 3.5%): terminal value ≈ ₹48,055.5 crore (undiscounted) → PV (discounted to today) ≈ ₹18,527.5 crore.

- Enterprise Value (PV FCFs + PV terminal): ≈ ₹28,446.3 crore.

- Add net cash (Investments − Borrowings ≈ ₹745 Cr) → Equity Value ≈ ₹29,191.3 crore.

- Shares outstanding: 40.4 crore → Fair value per share ≈ ₹722.6.

Base DCF fair value ≈ ₹723 / share (rounded).

Important: the DCF here is a simple, transparent walk-through — results are highly sensitive to growth, margins, discount rate, capex and NWC assumptions (see sensitivity table below).

D — Sensitivity (fair value per share) — discount rate × terminal growth

|

Discount rate ↓ \ Terminal growth → |

3.0% |

3.5% (base) |

4.0% |

|

9.0% |

₹819.1 |

₹871.2 |

₹933.8 |

|

10.0% |

₹687.7 |

₹722.6 |

₹763.2 |

|

11.0% |

₹590.2 |

₹614.5 |

₹642.3 |

(You can see how a small change in WACC or terminal growth swings per-share value materially.)

3) Interpretation & caveats (don’t skip these)

- The DCF base result (≈ ₹723/share) is well below the market price (market was ~₹2,484 on 8 Dec 2025). That gap can exist for several reasons: (a) the market is pricing in faster revenue growth or higher long-run margins than my base assumptions, (b) market expects very large transformational contracts (P-75I, LPD, upcoming submarine awards) that materially expand the order book beyond MDL’s FY25 visibility, (c) possible re-rating / strategic premium for defence PSUs, (d) one-time items or other income included in market valuations. Recent headlines (government OFS, large pipeline bids) also drive short-term price movements.

- My model is conservative on capex (3%) and assumes revenue growth 12% p.a.; if you believe MDL will win & execute very large new submarine/LPD contracts (or maintain higher margins), fair value would be much higher. Conversely, execution slippages or higher working capital needs reduce value.

- Model excludes non-operating items that may be in other income; I added investments − borrowings as a simple net cash adjustment (Screener values). For a fully audit-grade valuation we should use the company’s balance-sheet cash & equivalents, liquid investments, long-term liabilities, and incorporate lease liabilities / minority interests precisely.

4) Next steps I can do right now (pick any)

- Export the 10-year historical table + detailed year-by-year DCF projection to Excel/CSV and provide a download link. (I can produce the file in this chat.)

- Run alternative DCF scenarios (Conservative / Base / Aggressive) — e.g., growth 6% / 12% / 18% and show resulting fair values and sensitivity grids.

- Build a peer relative valuation (PE / EV/EBITDA vs other Indian shipyards / defence manufacturers) and show current implied multiples and re-rating scenarios.

Create a watchlist + dashboard of 6 KPIs to track quarterly (Order Book, Revenue YoY, EBIT margin, PAT, Receivables days, Cash conversion) and flag thresholds.

5. Risks & constraining factors

- Execution & delivery risk: Defence projects are capital and time intensive. Cost overruns, schedule slippages, or penalties can hit margins.

- Working capital & cash conversion: Large projects require high working capital; returns depend on milestone collections and contract terms.

- Regulatory / policy risk: Government decisions on procurement, offsets, or partner selection change project economics.

- Market/liquidity events: OFS or large promoter stake moves create supply pressure.

- Concentration risk: Heavy dependence on Indian defence budgets—slower defence spending would weigh on future revenue. (All stated risks are grounded in observed industry dynamics and recent MDL events.)

6. Valuation lens — simple approaches and caveats

- MDL is best valued using project-aware metrics: order-book adjusted revenue run-rate, execution margin assumptions, and discounted cash flows over multi-decade naval programmes. Relative multiples (PE, EV/EBITDA) can mislead because earnings are lumpy and influenced by contract phasing.

- For a quick public-market heuristic we can also use CAGR-projection of the share price under a set of assumed annual returns to generate long-term price scenarios. That is what I use below — a simple, transparent mathematical projection, not a DCF.

7. Share-price projections (baseline = ₹2,484.6 on 8 Dec 2025)

I present three scenarios (CAGR-based). Calculation method: FuturePrice = PresentPrice × (1 + CAGR) ^ years. (All figures rounded to nearest rupee or two decimals where helpful.)

Scenarios (annual CAGR assumed):

- Conservative = 6% p.a. (slow but steady growth)

- Base = 12% p.a. (reflects strong order-book execution and healthy margin expansion)

- Optimistic = 18% p.a. (outperformance — transformational contract wins + re-rating)

Computed projections (from baseline ₹2,484.60):

|

Year |

Years ahead |

Conservative (6%) |

Base (12%) |

Optimistic (18%) |

|

2025 (base) |

0 |

₹2,484.60 |

₹2,484.60 |

₹2,484.60 |

|

2030 |

5 |

₹3,324.96 |

₹4,378.71 |

₹5,684.16 |

|

2035 |

10 |

₹4,449.54 |

₹7,716.79 |

₹13,003.99 |

|

2050 |

25 |

₹10,663.58 |

₹42,238.36 |

₹155,706.47 |

(Numbers computed exactly from the CAGR formula and rounded to two decimals; baseline price sourced from market quotes on 8 Dec 2025).) Screener+1

How to read these: The Base (12%) scenario implies roughly a ~17x increase by 2050 from today’s price, reflecting a long multi-decade transformation driven by big defence programmes. The Conservative case shows modest compounding; the Optimistic shows very large re-rating if MDL captures and executes extremely large, high-margin contracts.

8. Why these scenarios might be realistic (or not)

- Support for upside: MDL’s FY21→FY25 revenue jump, strong order pipeline (Project-75I), and improved PAT prints in some quarters support faster growth if execution stays on track. Reports show large prospective submarine and warship contracts that could underpin multi-year revenue.

- Reasons to doubt upside: Delivery risks, contract renegotiations, funding / tax / policy changes, and short-term dilution from govt OFS could limit upside or produce volatility. Past quarters have proven profits can be lumpy — caution is required.

9. Suggested next analytical steps (if you want to go deeper)

If you ask, I can immediately produce (in this session):

- 10-year financial table: year-by-year Revenue / EBITDA / PAT / EPS / Order-Book (using audited numbers from annual reports / Moneycontrol) so you can compute historical CAGRs precisely.

- Simple DCF sketch: a defensible DCF (10-yr explicit + terminal value) using conservative margin and capex assumptions and MDL orderbook as revenue driver.

- Relative valuation: current EV/EBITDA or PE vs. listed peer shipyards / defence manufacturers and sensitivity table.

- Risk checklist & monitoring dashboard: items to watch (tender awards, OFS/tranche activity, quarterly collection & margin trends, working capital metrics).

Tell me which one you want and I’ll create it now (I’ll pull the latest audited figures and build the table and valuations in this chat). I will cite the specific annual reports and market pages used.

10. Final words (summary)

Mazagon Dock Shipbuilders is a core strategic defence asset with the potential for multi-year, multi-billion-dollar (₹-crore) contract flows that can materially increase revenues and shareholder value — but the path is lumpy. The CAGR-scenarios above provide a transparent mathematical baseline: they are not forecasts tied to a full valuation model, but useful for mapping outcomes under different growth assumptions. For actionable insight, the next step is a granular financial model (I can build that immediately with source citations).

Add a comment Cancel reply

Categories

- 3% Rule with AI (1)

- Alcoholic Beverages (1)

- Building Products – Pipes (1)

- Cement (2)

- Commodities Trading (1)

- Communication Sector Stocks (1)

- Communication Services (1)

- Consumer Finance (3)

- Consumer Staples (2)

- Energy Sector (1)

- Finance (1)

- FNO Calculator (3)

- Gas Distribution (1)

- Heavy Electrical Equipments (1)

- Heavy Machinery (1)

- Home Financing (1)

- How to Use FNO (3)

- Industrial Machinery (1)

- Investment (1)

- Investment Banking & Brokerage (2)

- Iron & Steel (1)

- IT Services & Consulting (5)

- Market Equity (1)

- Mining – Diversified (1)

- Oil & Gas – Refining & Marketing (1)

- Online Services (1)

- Pharmaceuticals (3)

- Power Infrastructure (1)

- Power Transmission & Distribution (1)

- Precious Metals, Jewellery & Watches (1)

- Private Banks (2)

- Renewable Energy (1)

- Retail – Apparel (1)

- Shipbuilding (1)

- Specialty Chemicals (2)

- Stationery (1)

- Stock Market News (23)

- Uncategorized (1)

Recent Posts

About us

Market Milestone

Blog Editor

Your Financial Milestone

with its super power, perfect financial appetite, Market Milestone gets you great stocks analysis, action packed calculator and learning on the go.

Popular Tags

Your Financial Milestone

with its super power, perfect financial appetite, Market Milestone gets you great stocks analysis, action packed calculator and learning on the go.